-

CALL US:

- (866) 952-3456

Think of your contracting business as a brand-new building. You've poured your time, money, and sweat into every last detail—your tools, your crew, your reputation with clients. What's holding it all up? The foundation.

That’s exactly what contractor insurance is. Without it, the whole structure you've built is at risk of crumbling.

It only takes one slip-up to bring on catastrophic costs. A ladder slides and wrecks a client's custom hardwood floors. An employee gets hurt on the job site. A company truck gets into a fender bender. Any of these can trigger a devastating lawsuit that could easily sink your business.

Having the right insurance isn't just about checking a legal box. It's the critical buffer standing between a manageable headache and a business-ending disaster.

Beyond just playing defense, the right insurance coverage is a powerful tool for building your reputation and landing better projects.

When you can hand over a Certificate of Insurance (COI), you're sending a clear message to potential clients: you're a professional who takes their investment seriously. It shows you've done your homework to protect their property, which can give you a major leg up on the competition.

In fact, many clients, especially on the commercial side, won't even look at a bid from a contractor who can't meet their minimum insurance requirements. Your coverage isn't just a safety net; it's the key that unlocks the door to bigger, higher-paying jobs.

In a high-risk industry like this, insurance stops being a simple expense and becomes your most strategic asset. It protects your finances, builds client trust, and gives you the solid ground you need to grow for the long haul.

You can see just how crucial this protection is by looking at industry trends. The global construction insurance market is on track to hit around $18.9 billion in 2025, a jump driven by increasing job site risks and more complex projects.

Even cyber insurance adoption among construction firms shot up by 26% in 2025 alone, showing that contractors are waking up to modern threats like data breaches and ransomware. You can discover more insights about these construction insurance statistics and trends to get the full picture.

At the end of the day, contractor insurance requirements aren't just hoops to jump through. They're guidelines designed to make the industry safer and more stable for everyone. By meeting them, you’re not just following the rules; you’re investing in the future of your own business.

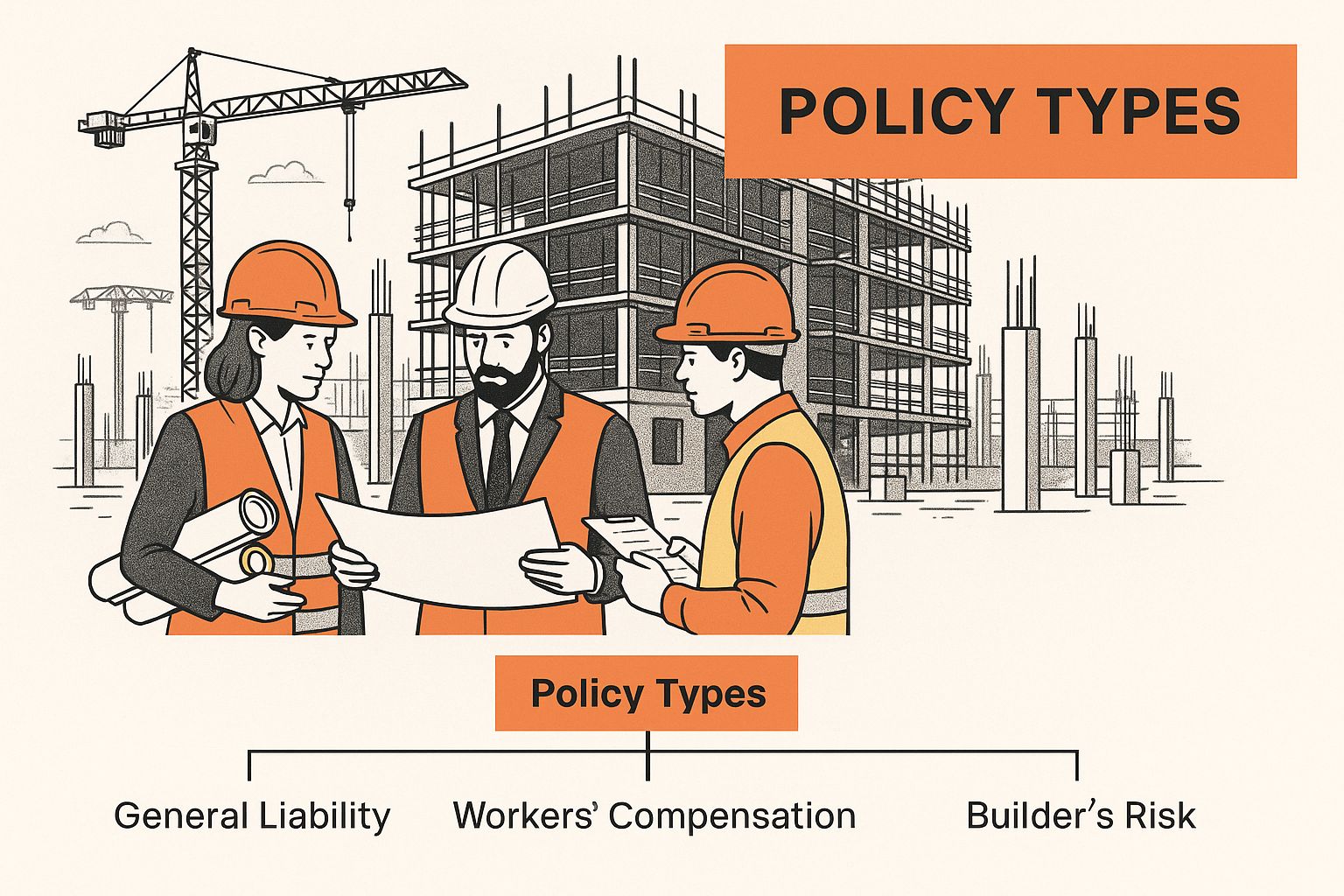

Trying to make sense of contractor insurance can feel like you’ve been handed a blueprint for a skyscraper when you were just trying to build a shed. It's complicated. Let's cut through the jargon and look at the core policies you'll actually need on the job site.

Think of each policy as a different tool in your toolbox—each one designed for a very specific job.

The image below breaks down the must-have policies that create your business’s safety net.

As you can see, every policy tackles a different kind of risk. From someone tripping over your tools to a fender bender in the work truck, you need a layered defense to protect your business from every angle.

Let's break down the essential policies every contractor should understand. To make it easier, here’s a quick overview of what we'll cover.

| Insurance Type | Primary Coverage | Who Needs It? |

|---|---|---|

| General Liability | Bodily injury or property damage to third parties (e.g., clients, visitors). | Virtually every contractor, especially those working on client property. |

| Workers' Compensation | Medical bills and lost wages for employees injured on the job. | Contractors with one or more employees (mandated in most states). |

| Commercial Auto | Liability and damage for vehicles used for business purposes. | Any contractor who drives a vehicle for work-related tasks. |

| Builder's Risk | Damage to a structure and materials during the course of construction. | General contractors, custom home builders, and remodelers. |

Now, let's dig into the details of what each of these policies actually does for you.

If there’s one policy you absolutely can’t operate without, it’s General Liability (GL). Think of it as your business’s first line of defense. It’s the policy that protects you from claims that you or your crew caused bodily injury or property damage to someone else—like clients, vendors, or just a random person walking by your job site.

This is almost always the first thing a client will ask for. No certificate of insurance, no job. Period.

Let’s play out a scenario that happens all the time. You’re a remodeler knee-deep in a kitchen gut. One of your guys accidentally drops a heavy nail gun, and it smashes a huge crack in the client’s brand-new, custom-installed quartz countertop. The client is furious and hands you a bill for a full replacement. We’re talking thousands of dollars.

Without General Liability, that money comes straight out of your pocket. With a GL policy, it’s designed to cover the cost of replacing that countertop, saving your business from a single, costly mistake.

General Liability insurance is non-negotiable. It’s the baseline coverage that addresses the everyday "what ifs" of property damage and third-party injuries, making it a fundamental part of your contractor insurance requirements.

And it's not just about paying for damage. A single lawsuit, even a frivolous one, can sink a small contracting business. The legal fees alone are enough to cause a world of pain. Your GL policy is designed to cover those legal defense costs, too.

While GL has your back with outsiders, Workers’ Compensation is all about protecting your own people. If an employee gets hurt or sick because of their job, this policy kicks in to cover their medical bills and pay them a portion of their lost wages while they’re out recovering.

Picture this: one of your roofers slips on a wet patch and falls from a ladder, breaking their leg. It’s a bad break, requiring an ER visit, surgery, and weeks of physical therapy. They’re going to be off the job for at least two months.

This is exactly what Workers' Comp is for.

Most states legally require you to carry Workers' Comp, even if you only have one employee. Getting caught without it can lead to massive fines, stop-work orders, and sometimes even criminal charges. It's an absolute must for any contractor with a crew.

A lot of contractors make the dangerous assumption that their personal auto insurance covers them for work. It doesn't. If you or an employee gets into an accident while driving for business—whether it's hauling tools, visiting a job site, or just making a run for materials—your personal policy will almost certainly deny the claim.

That’s where Commercial Auto insurance steps in. It’s built specifically for vehicles used for work, protecting you from liability if an accident causes injury or property damage to someone else. It's designed for the real-world risks of having vehicles on the road for your business.

For example, you’re driving your work truck and rear-end another car at a stoplight. Your commercial auto policy would help pay for the other driver’s medical bills and the repairs to their vehicle. You can’t meet your contractor insurance requirements without it, especially on commercial jobs where clients will demand to see proof of coverage.

You're six months into building a custom home. The framing is up, the windows are in, and you're ready to start the interior. Then, disaster strikes. A fire breaks out overnight from some temporary wiring, and half the structure is gone. Who pays to replace all that material and lost labor?

This is precisely what Builder's Risk insurance is for. It’s a temporary policy that protects the actual structure while it's under construction. It covers damage from things like fire, theft, vandalism, and bad weather. It’s there to protect both your and the owner’s financial stake in the project until it’s finished.

The market for this coverage is getting a bit more stable, but insurers are still cautious. Rates are still climbing, though not as steeply as before, as underwriters keep a close eye on risks like wildfires and major storms. You can read the full insurance marketplace analysis on WTWCo.com for a deeper dive. For any GCs doing new builds or major renovations, this policy is essential.

Getting a handle on your basic insurance policies is a solid first step. But the real puzzle is figuring out exactly what coverage you need to carry, because the rulebook changes depending on where you are and who you're working for.

Your specific insurance needs are really shaped by two big forces: the state you operate in, and the clients who hire you.

Think of state laws as the absolute minimum safety net for everyone in that area. They set the legal bar you have to clear just to be in business. On top of that, your clients often act like a demanding project manager, layering their own, much stricter requirements to protect their specific investment.

To stay compliant and actually win jobs, you’ve got to satisfy both.

Every state writes its own rulebook for contractors, and believe me, the differences can be huge. These laws are mostly about protecting workers and the public. Workers' Comp is the most common mandate you'll see, but the point at which it becomes required is all over the map.

For example, in California, you need Workers' Comp if you have even one single employee. Hop over to Mississippi, and that rule doesn't kick in until you have five or more people on your payroll. Then there’s Texas, which is a total outlier—it doesn't legally require most private companies to carry it at all, though you'd be crazy not to.

This same patchwork of regulations applies to licensing and general liability.

Here’s the bottom line: never assume the rules from one state apply to the next. You absolutely have to check with the official state licensing board before you even think about starting a project in a new location.

While the state sets the floor, your clients will almost always raise the ceiling. This is especially true when you're dealing with commercial jobs, government contracts, or big residential projects. The property owner or general contractor needs to know their investment is totally protected from any potential disaster.

So, what do they do? They spell out their exact insurance minimums right in the bid documents or service agreements. If you can't meet these client-driven requirements, your bid won't even get a second look.

It's pretty standard for clients to demand higher general liability limits, like $1 million per occurrence and a $2 million aggregate. They’ll also probably require you to add them to your policy as an “additional insured.” This just extends your liability coverage to protect them if they get dragged into a lawsuit because of something your crew did.

You might also see demands for specific commercial auto limits or even an umbrella policy for extra liability protection. For certain trades, like those offering plumbing services, the insurance mandates can get even more specific due to the higher-risk nature of their work.

So, where do you actually find all these all-important requirements? The good news is the information is usually right in front of you, as long as you know where to look.

Understanding the local market is also key, especially for specialized work. For instance, contractors providing services like furniture assembly in Dallas need to make sure their coverage not only meets Texas state guidelines but also fits what residential and commercial clients in that specific metro area expect. A little proactiveness here goes a long way in making sure you’re always ready to bid on—and win—your next big project.

Picking your insurance coverage can feel a lot like trying to order the exact amount of drywall for a job you haven't even walked yet. If you go too low, you're exposed. Go too high, and you're just burning cash on premiums you don't need. But figuring out the right coverage limits and deductibles isn't a guessing game—it's about making a smart call based on the real risks your business faces.

Think about it like your truck insurance. Your coverage limit is the max your insurance company will pay out if you cause a wreck. Your deductible is what you have to cough up first, out of your own pocket, before the insurance money starts flowing.

A higher limit gives you a bigger safety net, but it'll cost you more each month. On the flip side, a higher deductible can bring down that monthly premium, but it means you'll feel more of the financial sting upfront if something goes wrong. The sweet spot is finding that balance where your business is protected without killing your cash flow.

The right coverage isn't some off-the-shelf product; it has to fit the work you actually do. A painter working on empty residential interiors has a completely different risk profile than a roofer working three stories up on an occupied office building. You’ve got to be honest with yourself about your exposure.

Start by looking at a few key things:

Nailing down these variables helps you and your insurance agent land on a realistic level of protection that actually matches the contractor insurance requirements for your specific line of work.

If you've ever looked at a commercial contract, you've probably seen this line: $1 million per occurrence / $2 million aggregate. This is pretty much the industry standard for general liability, but what does it really mean?

Let’s break it down simply.

This structure is there to protect clients from both one single disaster and a string of smaller, costly mistakes. For anyone looking to land bigger, more profitable jobs, meeting this requirement is usually non-negotiable.

Balancing solid coverage with premiums you can actually afford is the name of the game. While global insurance rates saw a small dip, the U.S. market has stayed tough. That's because the costs and number of claims are rising, especially in the types of insurance that make up a contractor's general liability policy.

This just drives home how important a clean safety record is. You can't control what the market does, but you can control how an insurance company sees your business. The fewer claims you have, the better your negotiating position on premiums. You can learn more about the global insurance market trends on Marsh.com to get a feel for these forces.

At the end of the day, investing in good coverage isn't just about checking a box on a contract; it's about making sure your business can survive a worst-case scenario.

Trying to figure out why your insurance quote is what it is can feel like a mystery. But it’s not random—it’s a calculated risk assessment of your specific business. Insurers are looking at a whole range of factors to predict how likely you are to file a claim and what that claim might cost them.

Think of your premium as a direct reflection of your company's risk profile. The more risk an underwriter sees, the higher your premium will be. Simple as that. Some of these factors are out of your hands, but understanding what they are puts you back in control and gives you a roadmap to managing your costs over time.

First, insurers look at the absolute fundamentals of your operation. These core elements give them a baseline understanding of your day-to-day exposure to accidents and other liabilities.

Your Trade or Specialty: This is the big one. The type of work you do is easily the most significant factor. A roofer working three stories up faces a world of different risks than an interior painter. High-risk trades like electrical, plumbing, and demolition will almost always have higher premiums because of the inherent dangers.

Number of Employees: More people on the job means more chances for workplace injuries, which hits your workers' comp costs directly. Your total payroll is a key variable here; a bigger team simply increases the statistical odds of a claim.

Annual Revenue and Project Size: Bringing in more money usually means you’re taking on bigger, more complex, and higher-value projects. This cranks up your liability exposure. A mistake on a multi-million-dollar commercial build has wildly different financial consequences than a mishap on a small bathroom remodel.

After covering the basics, underwriters start digging into your company's actual track record. This is where you have the most direct impact on your rates.

Your claims history is a massive tell for insurers. A contractor with a history of frequent claims—even small ones—looks a lot riskier than one with a spotless record. Every claim signals a potential weak spot in your safety or work processes, and that translates to higher premiums.

This is exactly why having a proactive safety culture is so valuable. It’s not just fluff. Insurers genuinely favor businesses that can prove they’re serious about managing risk.

A documented safety program isn't just for show—it's a clear signal to insurers that you are actively working to prevent the very accidents they would have to cover. This commitment can translate directly into more favorable rates.

Putting formal safety protocols in place, running regular training sessions, and keeping a clean, organized job site are all tangible actions that lower your risk profile. When an underwriter sees a well-managed safety program, they see a better, safer investment. That can mean lower costs for you in the long run.

Your insurance premiums aren't set in stone. They're influenced by a mix of factors, from the type of work you do to the safety measures you implement. Here's a quick look at how different parts of your business can move the needle on your insurance costs.

| Factor | Impact on Premium | Example |

|---|---|---|

| High-Risk Trade | High | A roofing company will pay more than a landscaping business due to height-related risks. |

| Large Payroll | High | A construction firm with 50 employees has a higher workers' comp risk than a solo contractor. |

| Poor Claims History | High | Multiple liability claims in the past three years will significantly increase your general liability premium. |

| Large Project Values | Medium | A general contractor building commercial properties has more at stake than one doing small residential jobs. |

| Urban Location | Medium | Operating in a major city can increase rates due to higher litigation rates and property values. |

| Strong Safety Program | Low | Documented safety meetings and use of PPE can lead to discounts and lower premiums. |

| Years in Business | Low | An established business with 10+ years of clean history is seen as less risky than a startup. |

As you can see, both your operational focus and your commitment to safety play a huge role. By understanding these levers, you can make strategic decisions that not only protect your business but also help keep your insurance costs in check.

Finally, a few other operational choices you’ve made will help finalize your premium. Where your business is located matters, as some states have higher rates because of local laws and a greater tendency for lawsuits. Your years in business also play a part; a company with a proven, stable track record is often seen as less of a gamble than a brand-new operation.

Even the specific services you offer can have a surprising effect on what you pay. For instance, knowing the average furniture assembly service cost helps you price jobs, but an insurer also sees the liability in putting together complex items that could cause an injury if they fail. When you understand how all these pieces fit together, you can make smarter decisions to keep your insurance affordable and effective.

Trying to figure out contractor insurance can feel like you're staring at a mountain of paperwork and legal jargon. But if you break it down, getting the right coverage is a pretty straightforward project.

Think of it as a five-step plan to bulletproof your business. The goal is to get you from feeling uncertain to feeling confident, knowing you've got the exact protection you need to work safely and land those bigger, more profitable jobs.

Before you can even think about getting a quote, you need to get your ducks in a row. Insurance companies need a clear snapshot of your business to figure out your risk level.

Start by pulling together these essentials:

Next, take a hard, honest look at the real-world risks your business faces every day. The dangers for a roofer working three stories up are a world away from a painter worrying about overspray on a client's Lexus.

Think about the kinds of projects you typically handle, the value of the properties you're working on, and any heavy-duty equipment you use. This quick self-audit is huge—it helps you and your agent figure out exactly how much coverage you actually need.

Whatever you do, don't just call up the first agent in the phone book. You need someone who lives and breathes the construction world. An agent who specializes in contractors gets the unique liabilities you face and can translate those confusing client contracts into plain English. They're your most important partner in this whole process.

A specialist can spot coverage gaps a generalist would totally miss, making sure your policy checks all the boxes for state laws and client demands without costing you a fortune on stuff you don't need.

An agent who speaks the language of construction is your advocate. They don’t just sell you a policy; they help you build a comprehensive risk management strategy tailored to your specific trade and business goals.

Once the quotes start rolling in, fight the temptation to just grab the cheapest one. A low price often means low limits or, worse, critical exclusions that could leave your business dangerously exposed.

Instead, lay the policies out side-by-side. Look closely at the coverage limits, deductibles, and any policy exclusions. Does each quote meet the insurance requirements of your pickiest clients? The best deal isn't the cheapest policy; it's the one that gives you rock-solid protection at a fair price.

Okay, last step. Before you put ink to paper, read the fine print. This is your final chance to make sure everything is exactly right. Double-check that your business name is spelled correctly and that all the coverages you asked for, like additional insured endorsements, are actually in there.

After hiring your team, which you can streamline with a good contractor hiring checklist, this is one of the most important steps to protect your business. Once you’re 100% sure the policy is what you need, go ahead and sign. You're covered.

If you're a contractor, you've probably got a few questions about insurance. It's a world filled with confusing terms and requirements, but getting a handle on the basics is crucial for protecting your business and landing bigger jobs.

Lots of one-person operations wonder if they really need insurance. While you might be able to skip workers' comp if you don't have employees, general liability is absolutely essential. Think of it as a shield. It stands between a lawsuit from a worksite accident and your personal bank account, your home, and your savings. Besides, most clients won't even consider hiring you without it.

So, what’s a Certificate of Insurance, or COI? It’s just a one-page document that acts as your proof of insurance. It lays out what you're covered for, your policy limits, and the dates your coverage is active. Clients will always ask to see this before you set foot on their property.

A Certificate of Insurance is like your driver's license for contracting; it quickly proves you are authorized and safe to operate on a client's property, making it a critical tool for winning bids.

Another thing contractors ask about is how to save a little money. Bundling policies is often the way to go. A Business Owner’s Policy (BOP) is a great option here. It usually combines your general liability and commercial property insurance into one package, and it almost always costs less than buying them separately. For small to mid-sized contractors, it’s a smart, cost-effective move.

For those more specialized jobs, like putting together complex items, having the right, insured help is key. You can find professional support for tasks like putting together furniture, which ensures the project gets done right and safely. Find out more about how to get furniture assembly help for your next project.

Ready to get your furniture or equipment set up without the hassle? Assembly Smart offers professional, insured, and reliable assembly services for everything from IKEA desks to outdoor playsets. Get your free, upfront quote today and let our experts handle the setup, so you can enjoy your space. Visit us at https://assemblysmart.com to book your appointment.